When people hear the word mortgage, they usually think about a traditional home loan—borrowing money from a bank and paying it back over time. But sometimes you might come across unfamiliar legal terms like usufructuary mortgage. If you’re researching property laws, lending structures, or unusual mortgage arrangements in Indiana, you might be wondering: What exactly is a usufructuary mortgage, and does it even exist in Indiana law?

In this guide, we’ll break everything down in simple terms so you can understand what a usufructuary mortgage is, how it compares to common mortgage structures, and how property rights work in Indiana real estate law.

Whether you’re a homeowner, investor, law student, or just curious, this article will help you make sense of the topic.

Table of Contents

What Is a Usufructuary Mortgage?

Let’s start with the basics.

A usufructuary mortgage is a type of mortgage arrangement where the lender (or mortgagee) is given the right to possess and use the property—and collect income from it—until the loan is repaid.

The key concept here is usufruct.

In legal terms, usufruct means:

The right to use someone else’s property and enjoy the profits or benefits from it, while the ownership remains with the original owner.

So in a usufructuary mortgage, the borrower still owns the property, but the lender may temporarily take possession and benefit from the property’s income (such as rent or agricultural output) instead of receiving regular loan payments.

This concept appears more frequently in civil law systems and some foreign jurisdictions, particularly in parts of Asia, Latin America, and Europe.

But what about Indiana?

Does Indiana Recognize Usufructuary Mortgages?

Here’s where things get interesting.

Indiana does not formally recognize usufructuary mortgages under its mortgage law framework.

Indiana follows the lien theory of mortgages, which means:

- The borrower (mortgagor) keeps both legal and equitable title to the property.

- The lender (mortgagee) only holds a lien as security for the loan.

- The lender does not take possession of the property unless foreclosure occurs.

Because of this structure, a traditional usufructuary mortgage—where the lender takes possession and profits from the property—is not a typical or standard legal mortgage in Indiana.

Instead, Indiana real estate law uses more common financing structures, such as:

- Traditional mortgages

- Land contracts

- Deeds of trust (in some states)

- Lease-to-own agreements

- Seller financing arrangements

However, certain contractual agreements may sometimes resemble the economic effect of a usufructuary arrangement.

How Mortgages Normally Work in Indiana

To understand why usufructuary mortgages are unusual in Indiana, it helps to look at how standard mortgages operate in the state.

Indiana is a lien theory state, which means the mortgage works as security for a debt, not a transfer of property rights.

Here’s the basic structure:

- A borrower takes out a loan to purchase or refinance a property.

- The borrower signs a mortgage agreement giving the lender a lien.

- The borrower keeps possession and use of the property.

- The borrower makes monthly payments of principal and interest.

- If the borrower defaults, the lender may initiate judicial foreclosure.

In Indiana, foreclosures typically go through the court system, which protects the borrower’s rights and ensures due process.

Because the borrower retains possession during the loan term, there’s no built-in mechanism for a lender to collect profits directly from the property, which is a defining feature of usufructuary mortgages.

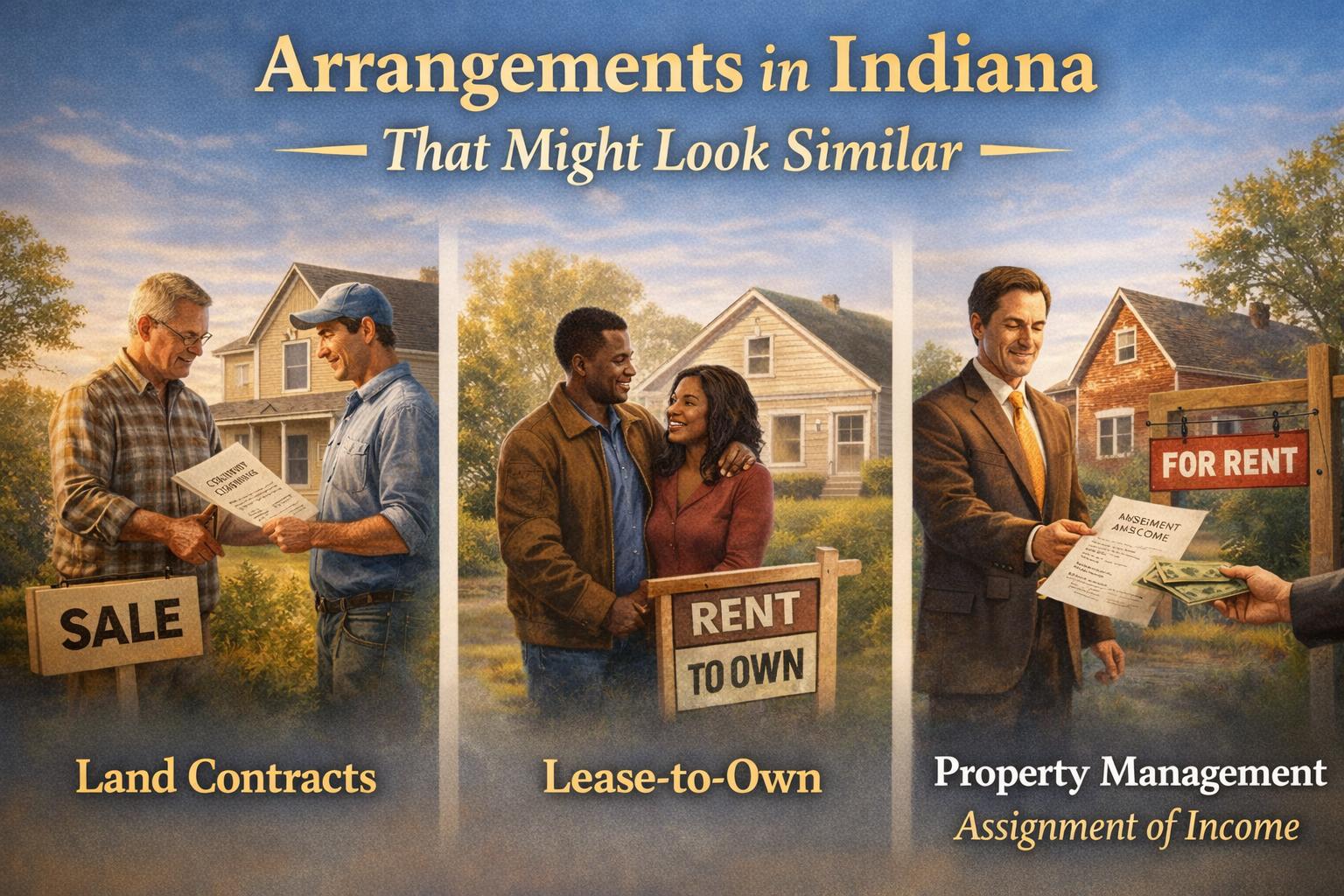

Arrangements in Indiana That Might Look Similar

Even though Indiana doesn’t formally use usufructuary mortgages, some creative financing arrangements can produce similar results.

Let’s explore a few examples.

1. Land Contracts (Contract for Deed)

A land contract is a seller-financing agreement where the buyer makes payments directly to the seller over time.

Key features include:

- The seller retains legal title until the contract is paid off.

- The buyer gains possession and use of the property.

- Payments are structured similarly to mortgage payments.

While this arrangement doesn’t allow the lender to collect income from the property directly, it can function as an alternative financing method when traditional mortgages are unavailable.

2. Lease-to-Own Agreements

Another structure sometimes compared to usufruct-style arrangements is lease-to-own.

In this setup:

- A tenant rents a property.

- A portion of rent may count toward the purchase price.

- The tenant has the option to buy later.

This isn’t a mortgage, but it does involve property use rights separate from ownership, which can resemble usufruct principles.

3. Property Management or Income Assignment

Sometimes lenders protect themselves by requiring an assignment of rents clause in a mortgage agreement.

This means:

- If the borrower defaults,

- The lender can collect rental income from tenants.

However, this only activates after default, not as a regular repayment method like in a usufructuary mortgage.

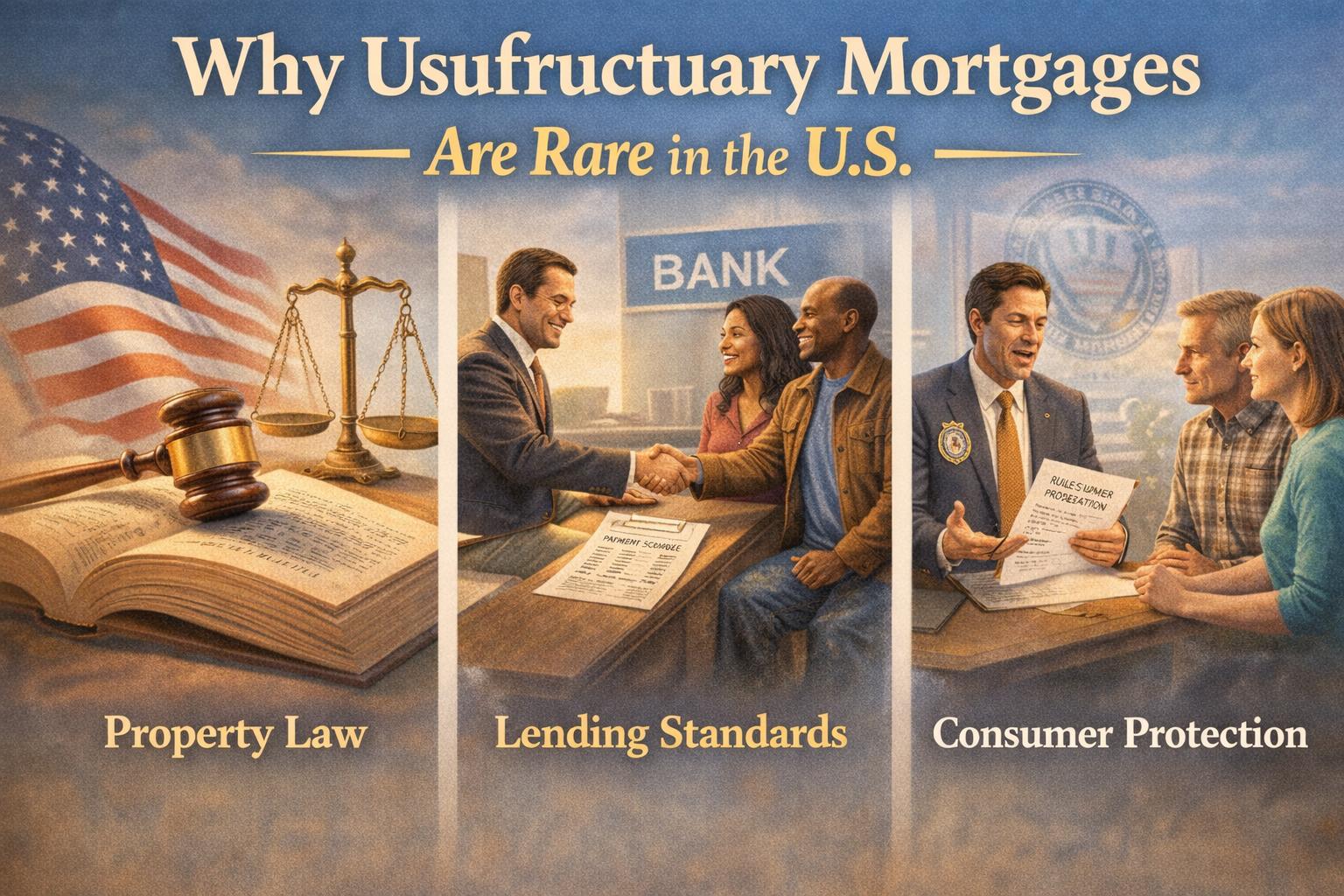

Why Usufructuary Mortgages Are Rare in the U.S.

The concept of usufructuary mortgages is uncommon in the United States for several reasons.

1. Property Law Structure

U.S. property law evolved under common law traditions, which treat mortgages primarily as security interests rather than possession-based arrangements.

This is very different from civil law systems where usufruct concepts are more common.

2. Lending Industry Standards

Modern mortgage lending is built around:

- monthly payments

- amortization schedules

- interest rates

- long-term financing

Allowing lenders to operate properties instead of collecting payments would complicate accounting, liability, and property management.

3. Consumer Protection Laws

U.S. states—including Indiana—have strong consumer protection laws that regulate lending practices.

Allowing lenders to take possession of homes during the loan period could create significant legal and ethical issues.

Could a Usufructuary-Type Agreement Be Created in Indiana?

Technically, parties in Indiana can create custom contractual agreements, but they must comply with:

- state property laws

- lending regulations

- foreclosure procedures

- consumer protection statutes

If a contract attempted to function exactly like a usufructuary mortgage, courts might interpret it differently depending on the circumstances.

In many cases, courts would likely treat it as:

- a lease agreement

- a management agreement

- or an equitable mortgage

Because of these legal complexities, anyone considering unusual real estate financing structures in Indiana should consult a qualified real estate attorney.

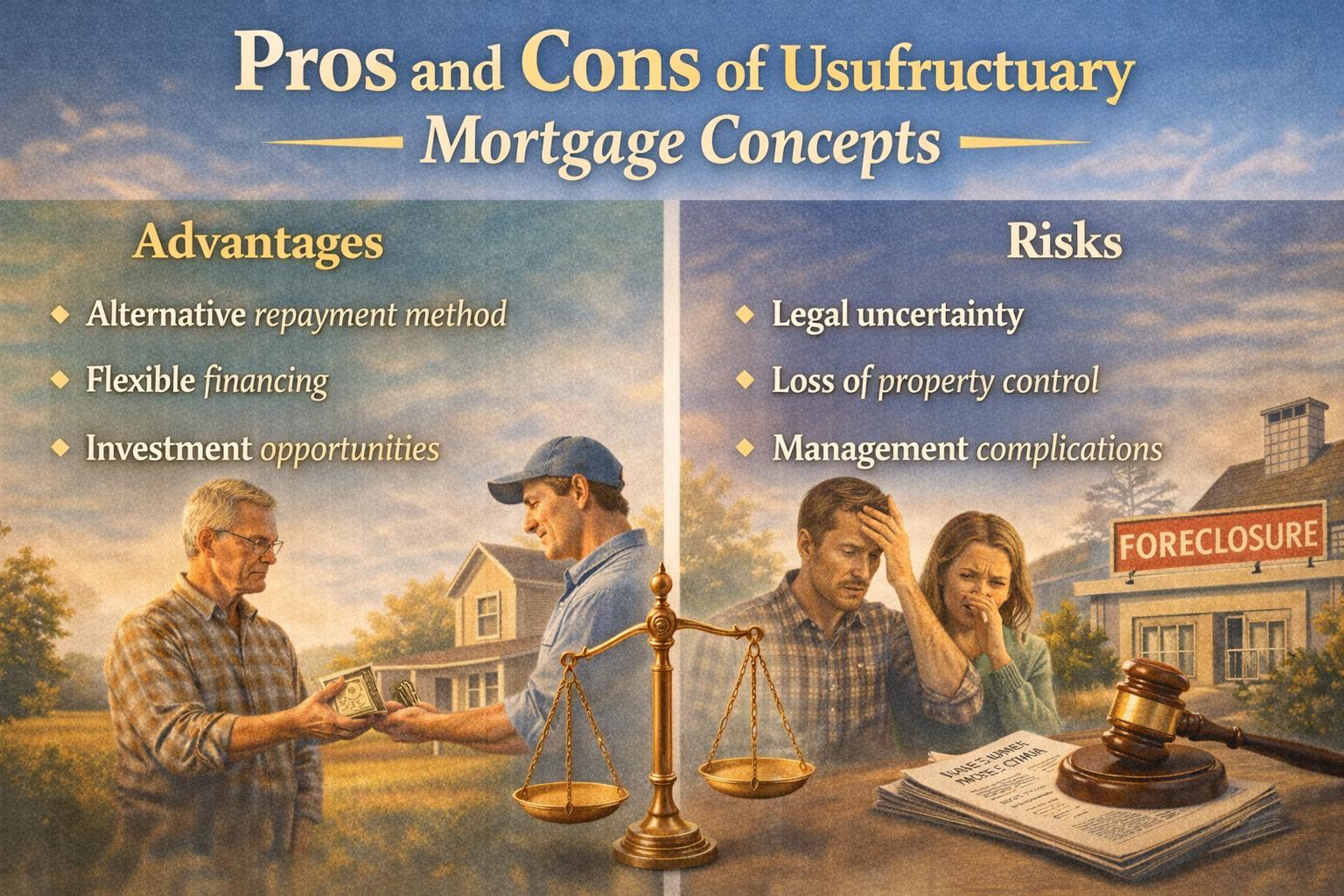

Pros and Cons of Usufructuary Mortgage Concepts

Even though they are not common in Indiana, it’s still useful to understand the potential advantages and disadvantages of usufructuary-style lending.

Potential Advantages

1. Alternative repayment method

Borrowers who cannot make traditional monthly payments might allow lenders to collect income from the property instead.

2. Flexible financing

These arrangements can sometimes help borrowers access financing when banks refuse loans.

3. Investment opportunities

In theory, lenders could generate income directly from property operations.

Potential Risks

1. Legal uncertainty

Because usufructuary mortgages are not standard in Indiana, courts may not enforce them the way parties expect.

2. Loss of property control

Borrowers could lose practical control of their property during the loan period.

3. Management complications

If a lender takes possession, they also assume responsibilities like maintenance, taxes, and liability risks.

Real Estate Advice for Indiana Property Owners

If you’re dealing with mortgages, property financing, or investment properties in Indiana, keep these tips in mind:

Understand your mortgage structure

Before signing any agreement, make sure you clearly understand:

- who owns the property

- who controls the property

- how repayment works

- what happens if you default

Work with qualified professionals

Real estate transactions often involve complex legal documents.

Consider consulting:

- a real estate attorney

- a mortgage professional

- a financial advisor

This helps ensure that agreements follow Indiana property law and protect your interests.

Be cautious with unconventional financing

Creative financing arrangements can be helpful in some situations, but they also come with risks.

If a deal sounds complicated or unusual, take extra time to review the legal implications.

Final Thoughts

While the term usufructuary mortgage in Indiana may appear in legal research or international property discussions, it is not a standard mortgage structure recognized under Indiana real estate law.

Indiana operates under a lien theory system, meaning borrowers retain possession and ownership while lenders hold a security interest in the property.

However, certain alternative financing arrangements—like land contracts, lease-to-own agreements, or rent assignments—can sometimes resemble aspects of usufruct-style property rights.

If you’re exploring unique property financing options, the most important step is ensuring that your agreement complies with Indiana law and protects both parties involved.

Real estate is one of the most significant financial commitments most people make, so taking the time to understand the legal details can save you from costly mistakes later.