Buying a home can feel exciting, overwhelming, and confusing all at the same time. If you’re planning to buy a house in Indiana, one term you might come across is a simple mortgage. While the phrase may sound technical, the concept is actually straightforward once you understand it.

In this simple guide, we’ll walk through what a simple mortgage in Indiana is, how it works, and what you should know before signing one. Whether you’re a first-time homebuyer or simply exploring your financing options, this article will help you make more confident decisions.

Table of Contents

What Is a Simple Mortgage?

A simple mortgage is a type of loan agreement where a borrower uses property as collateral to secure a loan. In most cases, this happens when someone takes out a loan to buy real estate.

Here’s the basic idea:

- You borrow money from a lender (usually a bank or mortgage company).

- You promise to repay the loan over time with interest.

- Your home or property acts as security for the loan.

If the borrower fails to repay the loan, the lender has the legal right to foreclose on the property and recover the unpaid balance.

While the term simple mortgage is often used in general discussions, in the United States—including Indiana—it typically refers to standard mortgage agreements used for residential property financing.

How a Simple Mortgage Works in Indiana

Understanding how a mortgage works can help you feel more prepared when entering the homebuying process.

In Indiana, the process usually looks like this:

1. Loan Application

You start by applying for a mortgage through a lender. During this stage, the lender reviews important details such as:

- Your credit score

- Income and employment

- Debt-to-income ratio

- Savings and down payment

The goal is to determine whether you can reliably repay the loan.

2. Property as Collateral

Once approved, the lender provides funds for the home purchase. In return, you sign a mortgage agreement stating that the property serves as collateral.

This means:

- You own the home

- The lender holds a lien on the property until the loan is fully paid

3. Monthly Mortgage Payments

Most mortgages in Indiana are repaid through monthly payments that include:

- Principal (the amount you borrowed)

- Interest (the cost of borrowing)

- Property taxes

- Homeowners insurance

These payments typically last 15 to 30 years, depending on your loan term.

4. Loan Completion or Foreclosure

If you successfully pay off the loan, the lender releases the lien and you fully own the property.

However, if payments stop for an extended period, the lender may begin foreclosure proceedings, which allows them to sell the home to recover the loan balance.

Why Simple Mortgages Are Popular in Indiana

Indiana is known for its affordable housing market, which makes homeownership more accessible compared to many other states.

Because of this, simple mortgage structures are commonly used by homebuyers across the state.

Some key reasons include:

Affordable Housing Prices

Indiana’s median home prices are often lower than the national average. This allows many buyers to qualify for mortgages with manageable monthly payments.

Flexible Loan Programs

Many lenders in Indiana offer a variety of mortgage options, including:

- Conventional loans

- FHA loans

- VA loans

- USDA rural development loans

These programs make it easier for different types of buyers to enter the housing market.

Predictable Payment Plans

With fixed-rate mortgages, homeowners can enjoy consistent monthly payments, which helps with budgeting and financial planning.

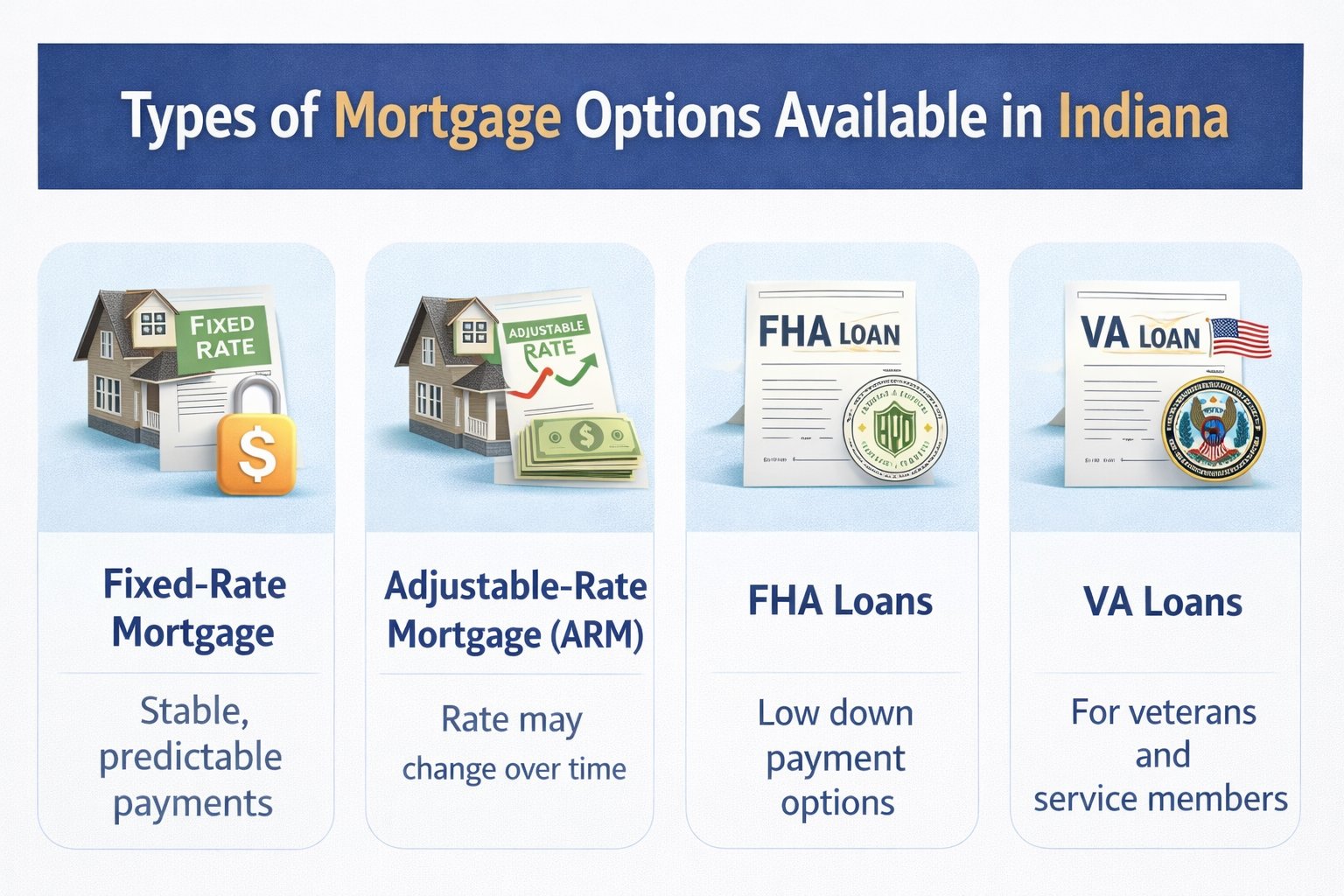

Types of Mortgage Options Available in Indiana

While a simple mortgage structure is common, borrowers can choose from several loan types depending on their financial situation.

Fixed-Rate Mortgage

This is one of the most popular options.

With a fixed-rate mortgage, the interest rate remains the same throughout the entire loan term.

Benefits include:

- Predictable monthly payments

- Long-term financial stability

- Protection from rising interest rates

Most buyers choose 15-year or 30-year fixed loans.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a lower interest rate that may change over time.

For example:

- The first 5 years may have a fixed rate

- After that, the rate adjusts annually

While ARMs can offer lower initial payments, they also come with potential interest rate increases later.

FHA Loans

FHA loans are backed by the Federal Housing Administration and are designed for buyers with lower credit scores or smaller down payments.

Many first-time buyers in Indiana use FHA loans because they allow:

- Down payments as low as 3.5%

- More flexible credit requirements

VA Loans

If you’re a veteran or active-duty service member, you may qualify for a VA loan.

These loans often offer:

- No down payment

- Lower interest rates

- No private mortgage insurance (PMI)

USDA Loans

For buyers looking at homes in rural areas of Indiana, USDA loans may be available.

These loans offer:

- Zero down payment options

- Lower mortgage insurance costs

- Competitive interest rates

Key Legal Aspects of Mortgages in Indiana

Indiana has specific laws that affect how mortgages and foreclosures are handled.

Here are a few important points to know.

Judicial Foreclosure State

Indiana is considered a judicial foreclosure state.

This means lenders must go through the court system before they can foreclose on a property.

While foreclosure is still serious, the judicial process can provide borrowers with additional time and legal protections.

Redemption Period

Indiana may allow a limited redemption period, which gives borrowers a chance to pay off the loan balance and reclaim their property before the foreclosure sale is finalized.

However, the rules can vary depending on the case.

Mortgage Recording

When a mortgage is created, it must be recorded with the county recorder’s office.

This public record ensures that the lender’s claim on the property is legally recognized.

Tips for Getting a Simple Mortgage in Indiana

If you’re planning to apply for a mortgage in Indiana, preparation can make the process much smoother.

Here are some helpful tips.

Improve Your Credit Score

Your credit score plays a major role in determining your mortgage terms.

A higher score can help you secure:

- Lower interest rates

- Better loan options

- Reduced mortgage costs over time

Paying bills on time and reducing existing debt can improve your score before applying.

Save for a Down Payment

Although some loans require little or no down payment, saving at least 5%–20% of the home price can improve your approval chances.

A larger down payment may also eliminate private mortgage insurance.

Compare Multiple Lenders

Not all lenders offer the same mortgage terms.

Before committing, compare several lenders to evaluate:

- Interest rates

- Closing costs

- Loan fees

- Customer reviews

Even a small interest rate difference can save thousands over the life of the loan.

Understand the Total Cost of Ownership

Owning a home involves more than just mortgage payments.

You should also budget for:

- Property taxes

- Home maintenance

- Insurance

- Utilities

Planning for these expenses helps avoid financial stress later.

Get Pre-Approved Before House Hunting

Mortgage pre-approval shows sellers that you’re a serious buyer.

It also helps you understand how much home you can realistically afford.

In competitive housing markets, pre-approval can give you a major advantage.

Common Mistakes to Avoid

Many first-time buyers make mistakes during the mortgage process.

Here are a few to watch out for.

Taking on Too Much Debt

Just because a lender approves a certain amount doesn’t mean you should borrow the maximum.

Choose a mortgage payment that fits comfortably within your monthly budget.

Ignoring Loan Details

Always read the fine print before signing any mortgage agreement.

Pay attention to:

- Interest rate terms

- Prepayment penalties

- Adjustable rate conditions

Understanding these details can prevent surprises later.

Skipping the Home Inspection

A mortgage approval doesn’t guarantee that the home is in good condition.

Hiring a professional home inspector can help you avoid costly repairs after moving in.

Final Thoughts

A simple mortgage in Indiana is essentially the standard way most homeowners finance their property. While the concept may sound complicated at first, it simply involves borrowing money to purchase a home while using that property as collateral.

The key to success is understanding your options, preparing your finances, and choosing the right lender.

Indiana remains one of the more affordable states for homebuyers, making it an attractive place to settle down and invest in real estate. With the right planning and knowledge, securing a mortgage can be a smooth and rewarding step toward homeownership.

If you’re considering buying a home in Indiana, take the time to research mortgage options, compare lenders, and make sure the loan you choose fits your long-term financial goals.

After all, a home is more than just a purchase—it’s where your future memories will be made.