The Complete Guide to USDA Mortgage Loans in Indiana (2026 Edition)

How everyday Hoosiers are buying homes with zero down—and how you can too

If you’ve ever thought buying a home in Indiana required a massive down payment, perfect credit, and years of saving, you’re not alone. That belief stops a lot of people from even trying. But here’s the reality: there’s a powerful home loan program designed specifically for people like you—people who want a home, not a financial headache.

It’s called the USDA mortgage loan, and for many Indiana residents, it’s one of the most accessible, affordable, and overlooked ways to become a homeowner.

This isn’t some niche or complicated government program reserved for a select few. In fact, thousands of families across Indiana—from small towns to suburban edges—have used this loans to buy homes with zero down payment and surprisingly flexible requirements.

In this guide, I’ll walk you through everything you need to know—from how this loans actually work, to who qualifies in Indiana, to real-life scenarios that show how this loan can change your situation.

Let’s break it down.

Table of Contents

What Is a USDA Mortgage Loan?

A USDA loan is a home loan backed by the United States Department of Agriculture. While the name might sound like it’s only for farmers, that’s one of the biggest misconceptions.

This loans are actually designed to help low-to-moderate income individuals and families purchase homes in eligible rural and suburban areas.

And here’s the key part:

👉 “Rural” doesn’t mean remote farmland.

In Indiana, many suburban communities—even areas near cities like Indianapolis, Fort Wayne, and Evansville—qualify as USDA-eligible zones.

Why USDA Loans Are So Popular in Indiana

Indiana is one of the best states in the country for this loans, and here’s why:

1. Huge Areas Qualify

A large portion of Indiana falls under USDA eligibility maps. That means you’re not limited to isolated countryside—you have real choices.

2. Affordable Housing Market

Compared to coastal states, Indiana’s home prices are more accessible. Combine that with zero down, and homeownership becomes realistic.

3. Strong Fit for Middle-Income Families

This loans are perfect for:

- First-time homebuyers

- Families upgrading from renting

- People relocating to quieter communities

The Biggest Advantage: Zero Down Payment

Let’s start with the feature everyone cares about:

👉 You can buy a home with $0 down.

Yes, really.

With a this loan, you don’t need the typical:

- 3% (conventional)

- 3.5% (FHA)

- 5–20% (traditional expectations)

Instead, this allows you to finance 100% of the home’s value.

What This Means in Real Life

Imagine a $220,000 home in Indiana.

- Conventional loan (5% down): $11,000 upfront

- FHA loan (3.5% down): $7,700 upfront

- USDA loan: $0 down

That’s a massive difference—especially if saving is your biggest obstacle.

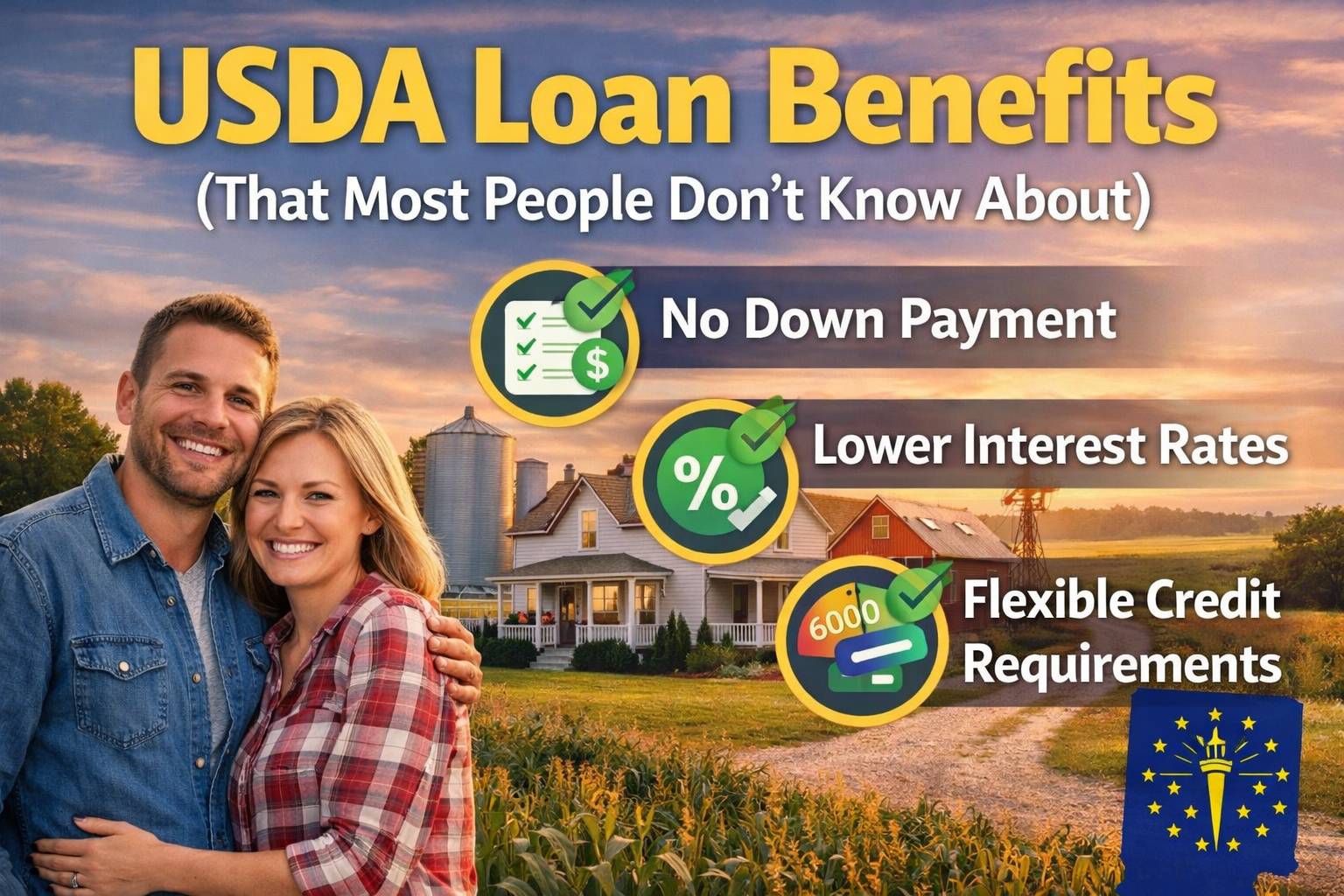

USDA Loan Benefits (That Most People Don’t Know About)

Zero down is just the beginning.

1. Lower Monthly Payments

This loans often come with competitive interest rates, sometimes lower than conventional loans.

2. Reduced Mortgage Insurance

Instead of traditional PMI, USDA loans have:

- Lower upfront fee

- Lower monthly fee

This can save you hundreds per year.

3. Flexible Credit Requirements

You don’t need perfect credit.

While lenders vary, many USDA borrowers qualify with:

- Credit scores in the 620+ range

- Even lower in some cases with compensating factors

4. Seller Can Cover Closing Costs

Yes—you can potentially buy a home with:

- $0 down

- Minimal out-of-pocket costs

Who Qualifies for a USDA Loan in Indiana?

Let’s simplify it.

There are three main requirements:

1. Location Eligibility

The home must be in a USDA-eligible area.

Good news:

👉 Most of Indiana qualifies.

Eligible areas include:

- Small towns

- Suburbs outside major cities

- Semi-rural communities

Even areas just outside:

- Indianapolis

- South Bend

- Bloomington

…often qualify.

2. Income Limits

This loans are designed for low-to-moderate income households.

In Indiana, income limits vary by county and household size, but generally:

- 1–4 person household: around $110,000–$120,000 max

- 5+ people: higher limits

These are not “low income” in the traditional sense—many middle-class families qualify.

3. Credit & Financial Stability

You don’t need perfect finances, but lenders look for:

- Stable income

- Manageable debt

- Reasonable credit history

Typical guidelines:

- 620+ credit score preferred

- Debt-to-income ratio around 41% or lower

What Kind of Homes Can You Buy?

This loans are meant for primary residences, not investment properties.

Eligible properties include:

- Single-family homes

- New construction homes

- Some condos (if approved)

- Manufactured homes (with restrictions)

The home must be:

- Safe

- Livable

- Modest in size

No luxury mansions—but plenty of great homes.

Real-Life Example: USDA Loan in Indiana

Let’s make this real.

Meet Jake and Sarah (Fictional, but realistic)

- Location: Lafayette, Indiana

- Combined income: $78,000

- Savings: $4,000

- Credit score: 640

They assumed they needed years to save for a house.

Instead, they used a this loan and:

- Bought a $210,000 home

- Paid $0 down

- Had the seller cover most closing costs

Their monthly payment? Comparable to their rent.

USDA Loan vs FHA vs Conventional

Here’s how USDA compares:

| Feature | USDA | FHA | Conventional |

|---|---|---|---|

| Down Payment | 0% | 3.5% | 3–20% |

| Credit Flexibility | Moderate | Flexible | Stricter |

| Mortgage Insurance | Lower | Higher | Varies |

| Location Restriction | Yes | No | No |

👉 If you qualify, this is often the most affordable option.

Step-by-Step: How to Get a USDA Loan in Indiana

Let’s walk through the process.

Step 1: Check Eligibility

Start by confirming:

- Your income fits limits

- The area qualifies

A lender can quickly help with this.

Step 2: Get Pre-Approved

This is crucial.

A lender will:

- Review your credit

- Calculate your budget

- Issue a pre-approval letter

This makes you a serious buyer.

Step 3: Find a USDA-Eligible Home

Work with a real estate agent familiar with this loans.

They’ll help you:

- Identify eligible areas

- Avoid properties that won’t pass inspection

Step 4: Make an Offer

Once you find a home:

- Submit your offer

- Negotiate terms (including closing costs)

Step 5: Underwriting & USDA Approval

This part has two approvals:

- Lender approval

- USDA approval

It can take slightly longer—but it’s manageable.

Step 6: Close and Get the Keys

Once approved:

- Sign documents

- Finalize loan

- Move in 🎉

Common Misconceptions About USDA Loans

Let’s clear these up.

“It’s only for farmers”

Not true. Most borrowers are regular homebuyers.

“The homes are in the middle of nowhere”

Also false. Many suburban areas qualify.

“The process is too complicated”

It’s slightly more detailed—but very doable with the right lender.

“You have to be low income”

No—you just need to fall under moderate income limits.

Pros and Cons of USDA Loans

Pros

- No down payment

- Lower monthly costs

- Flexible credit requirements

- Accessible for first-time buyers

Cons

- Location restrictions

- Income limits

- Slightly longer approval process

Tips for Getting Approved Faster

If you’re serious about using this loan in Indiana, here’s how to improve your chances:

1. Improve Your Credit Score

Even a small boost can help your rate.

2. Reduce Debt

Lower debt = higher approval odds.

3. Work With a USDA-Experienced Lender

Not all lenders are equal.

4. Have Stable Employment

Consistency matters more than high income.

Is a USDA Loan Right for You?

It might be perfect if:

- You don’t have a large down payment

- You’re open to suburban or rural living

- Your income falls within limits

- You want lower monthly payments

It may not be ideal if:

- You’re buying in a major urban center

- Your income exceeds limits

The Indiana Advantage

Indiana stands out for this loans because:

- Housing is still affordable

- Many areas qualify

- Cost of living is manageable

This combination makes it one of the best states to use this program effectively.

Final Thoughts: Why More People Should Consider USDA Loans

Here’s the truth most people don’t hear:

You don’t need to wait years to buy a home.

You don’t need perfect credit.

You don’t need a massive savings account.

Programs like this loans exist because homeownership is still meant to be achievable—not just for the wealthy, but for everyday people.

And in a state like Indiana, where the market is still relatively accessible, the opportunity is even bigger.

What You Should Do Next

If this sounds like something that could work for you:

- Talk to a USDA-approved lender

- Check your eligibility

- Get pre-approved

- Start exploring homes

You might be closer to owning a home than you think.

Bottom line:

This loan isn’t just a mortgage—it’s a shortcut past one of the biggest barriers to homeownership: the down payment.

And for many Indiana residents, it’s the opportunity they didn’t realize they had.