Buying a home is one of the biggest milestones in life. It’s exciting, but let’s be honest—it can also feel overwhelming, especially when you start hearing terms like pre-approval, underwriting, and closing costs. If you’re planning to buy a home in Indiana, understanding the 5 stages of a mortgage can make the entire process much less stressful.

Think of a mortgage like a journey. Each stage moves you one step closer to holding the keys to your new home. When you know what’s coming next, you can prepare better, avoid common mistakes, and feel more confident throughout the process.

In this guide, we’ll walk through the five stages of a mortgage in Indiana, explain what happens during each stage, and share helpful tips to make the process smoother. Whether you’re a first-time homebuyer or someone who hasn’t purchased a home in years, this guide will help you understand how mortgages work in Indiana.

Table of Contents

Understanding the Mortgage Process in Indiana

Before diving into the stages, let’s briefly talk about how mortgages work.

A mortgage is simply a loan that helps you purchase a home. Because most people don’t have hundreds of thousands of dollars available to buy a home outright, lenders (such as banks or mortgage companies) provide financing. In return, you agree to repay the loan over time—usually 15 to 30 years—with interest.

In Indiana, the mortgage process follows the same general structure as the rest of the United States, but there are some local considerations like property taxes, loan programs, and state-specific closing procedures.

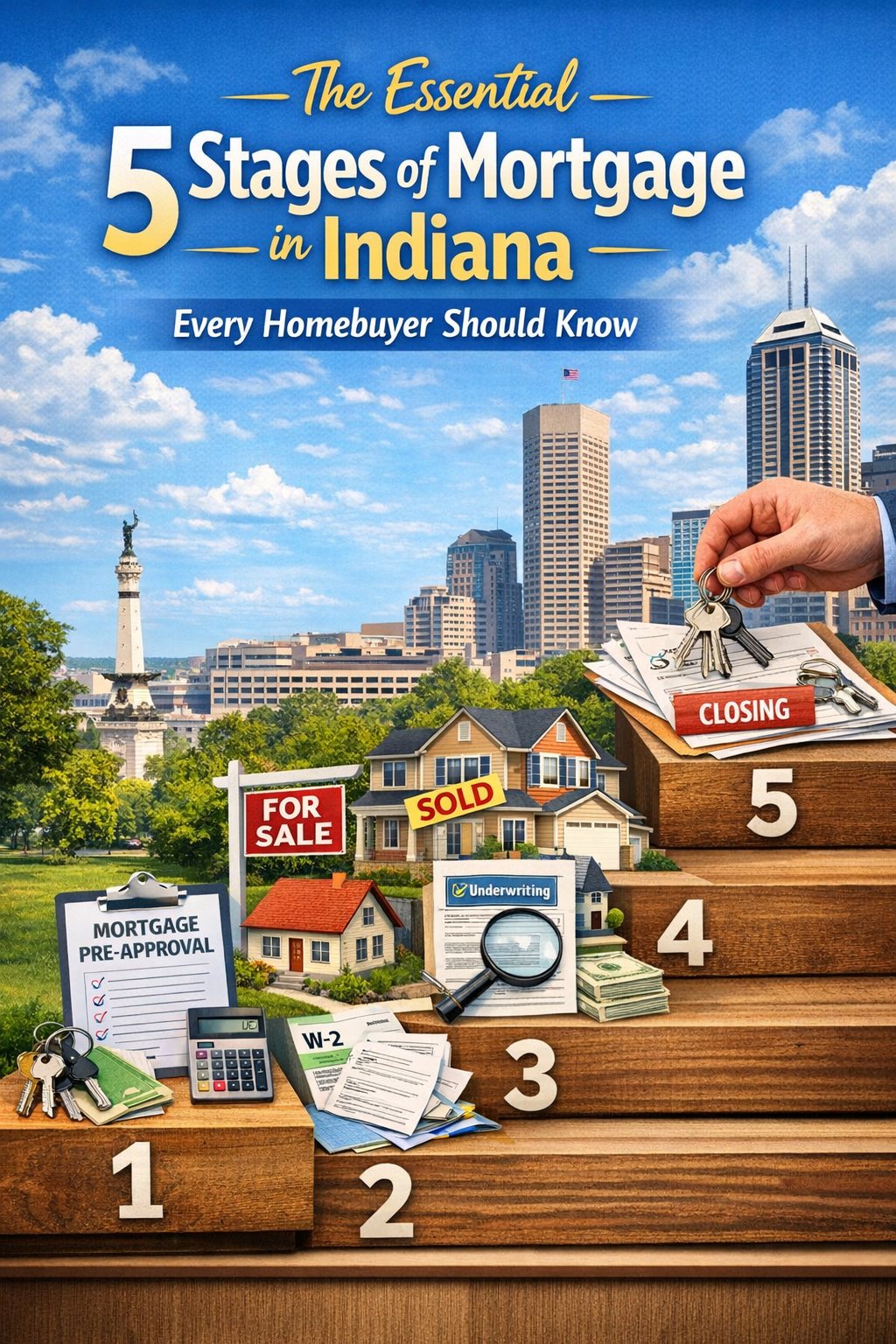

The mortgage journey typically involves five main stages:

- Mortgage Pre-Approval

- House Hunting and Offer

- Mortgage Application

- Loan Processing and Underwriting

- Closing on Your Indiana Home

Let’s explore each stage in detail so you know exactly what to expect.

Stage 1: Mortgage Pre-Approval

The first stage of getting a mortgage in Indiana is mortgage pre-approval. This step happens before you start seriously shopping for a home.

Many first-time buyers skip this stage, but it’s actually one of the most important parts of the entire process.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is when a lender reviews your financial information to determine how much money they’re willing to lend you for a home purchase.

During this step, the lender evaluates things like:

- Your credit score

- Your income and employment history

- Your debt-to-income ratio

- Your assets and savings

If everything looks good, the lender will give you a pre-approval letter, which shows sellers that you’re a serious buyer who can afford the home.

Why Pre-Approval Matters in Indiana

Indiana’s housing market can vary depending on the city. For example:

- Indianapolis often has competitive housing markets.

- Fort Wayne and Evansville may have more affordable options.

- Smaller towns may offer lower prices but fewer available homes.

A pre-approval letter helps you stand out to sellers in competitive markets and prevents you from wasting time looking at homes outside your budget.

Documents You’ll Typically Need

To get pre-approved for a mortgage in Indiana, lenders usually ask for:

- Recent pay stubs

- W-2 forms from the last two years

- Tax returns

- Bank statements

- Identification

- Employment verification

Providing these documents helps lenders verify that you’re financially capable of repaying the loan.

Tips for a Smooth Pre-Approval Process

Here are some simple tips that can help you get pre-approved faster:

1. Check your credit score first

If your credit score needs improvement, it’s better to fix it before applying.

2. Avoid large purchases

Buying a car or taking on new debt can affect your loan approval.

3. Save for a down payment

Many Indiana lenders prefer buyers to have 3%–20% down, depending on the loan type.

4. Compare lenders

Different lenders offer different rates and loan programs.

Pre-approval sets the foundation for the entire mortgage process. Once you have it, you’re ready to move on to the exciting part—finding your home.

Stage 2: House Hunting and Making an Offer

Once you’re pre-approved, the next stage of the mortgage process in Indiana is finding the right home and making an offer.

This is usually the most exciting stage because you finally get to imagine yourself living in your future home.

Finding the Right Home in Indiana

Indiana offers a wide range of housing options, including:

- Single-family homes

- Townhouses

- Condos

- Rural properties

- New construction homes

Home prices in Indiana are generally lower than the national average, which makes the state attractive for first-time buyers and families.

However, it’s still important to consider factors like:

- Neighborhood safety

- School districts

- Commute times

- Property taxes

- Future resale value

Working with a local Indiana real estate agent can make a huge difference. They understand the market and can guide you toward homes that fit your budget and goals.

Making an Offer on a Home

When you find a home you love, your real estate agent will help you submit an offer.

The offer typically includes:

- Purchase price

- Earnest money deposit

- Closing timeline

- Contingencies (inspection, financing, appraisal)

In Indiana, earnest money is often between 1% and 3% of the purchase price. This deposit shows the seller you’re serious about buying.

Home Inspection

Before moving forward with the mortgage, most buyers schedule a home inspection.

An inspector checks the property for potential problems like:

- Roof damage

- Plumbing issues

- Foundation problems

- Electrical hazards

If major issues are discovered, you may negotiate repairs with the seller or adjust the purchase price.

Why This Stage Matters for Your Mortgage

Lenders won’t approve your mortgage without a signed purchase agreement. Once your offer is accepted, you officially move to the next step—the formal mortgage application.

Stage 3: Mortgage Application

After your offer is accepted, it’s time to officially apply for your mortgage loan.

This is where the mortgage process becomes more detailed, and lenders start carefully evaluating your financial situation.

What Happens During the Mortgage Application?

During the mortgage application stage, you’ll provide detailed financial information to your lender.

Your lender will collect documents such as:

- Proof of income

- Credit reports

- Bank statements

- Employment verification

- Property information

The goal is to confirm that you qualify for the mortgage you’re requesting.

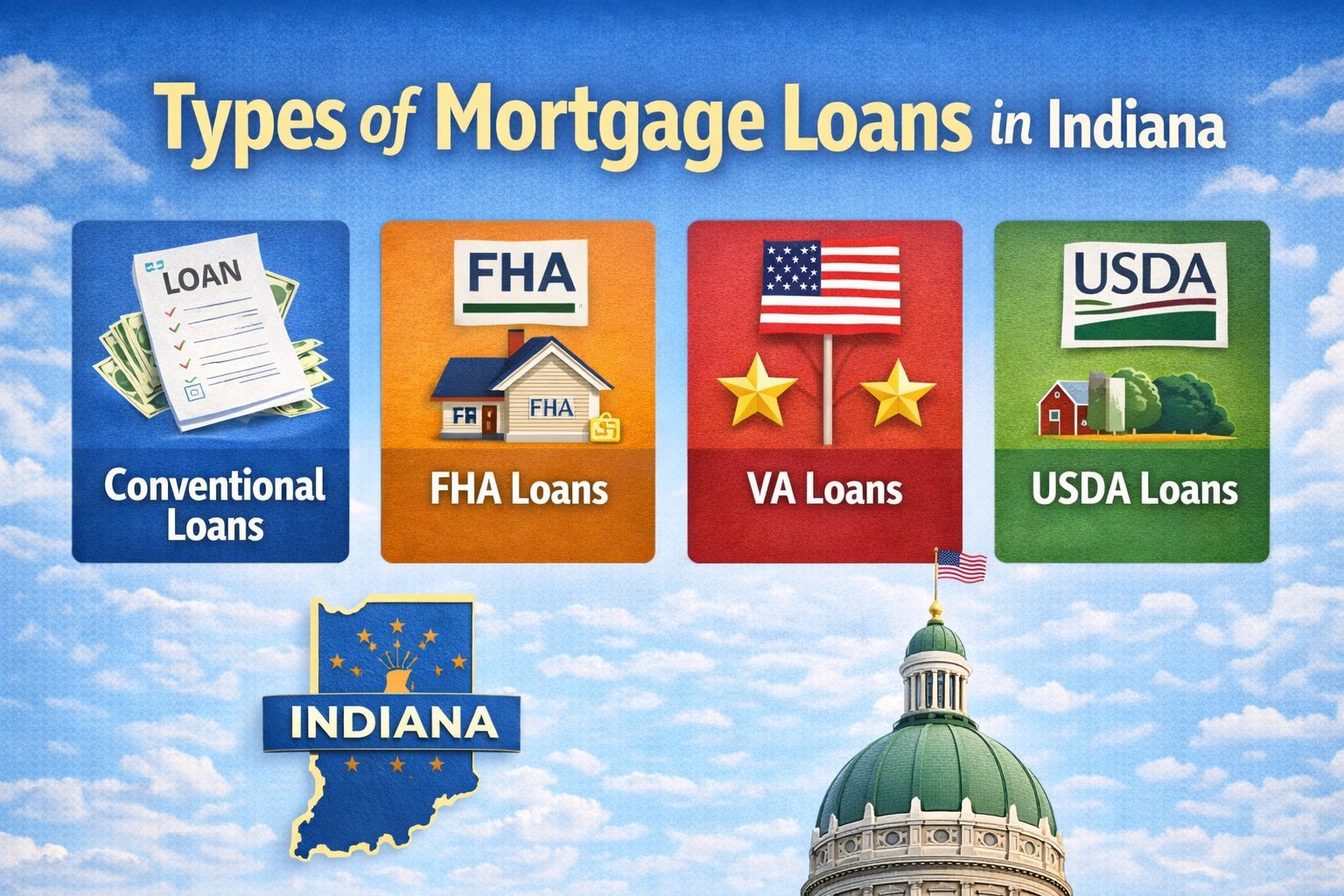

Types of Mortgage Loans in Indiana

Several loan programs are available to Indiana homebuyers. Some of the most common include:

Conventional Loans

These loans are not backed by the government and usually require higher credit scores.

FHA Loans

FHA loans are popular among first-time buyers because they allow lower down payments and more flexible credit requirements.

VA Loans

Available to veterans and active military members, VA loans often require no down payment.

USDA Loans

These loans are designed for rural areas and may offer 100% financing.

Indiana also offers special assistance programs through the Indiana Housing and Community Development Authority (IHCDA) that help first-time buyers with down payments and closing costs.

Locking Your Interest Rate

During the application stage, you may choose to lock your interest rate.

This means your rate won’t change even if mortgage rates increase before closing.

Rate locks typically last 30 to 60 days, which is usually enough time to complete the mortgage process.

Stage 4: Loan Processing and Underwriting

Once you submit your mortgage application, your loan enters the processing and underwriting stage.

This is often the longest stage of the mortgage process, but it’s also one of the most important.

What Is Loan Processing?

Loan processors gather and organize all the documents needed for underwriting.

They verify:

- Your income

- Employment

- Credit history

- Bank accounts

- Property details

They may also request additional documents if something needs clarification.

The Home Appraisal

Another important part of this stage is the home appraisal.

An appraiser determines the fair market value of the property to ensure the home is worth the amount you’re borrowing.

If the appraisal comes in lower than the purchase price, you may need to:

- Renegotiate with the seller

- Increase your down payment

- Cancel the deal

What Is Underwriting?

Underwriting is when a mortgage professional reviews all the information to determine if the loan should be approved.

Underwriters assess the risk of lending money to you.

They examine factors such as:

- Credit score

- Debt-to-income ratio

- Income stability

- Property value

If everything meets the lender’s guidelines, your loan will receive conditional approval.

Sometimes the underwriter may request additional documentation before giving final approval.

How Long This Stage Takes

In Indiana, the underwriting process usually takes 1 to 3 weeks, though it can vary depending on the lender and complexity of the loan.

Patience is important during this stage because it brings you closer to closing.

Stage 5: Closing on Your Indiana Home

The final stage of the mortgage process is closing.

This is the day when ownership of the property officially transfers from the seller to you.

What Happens During Closing?

At closing, you’ll review and sign several legal documents related to your mortgage and property purchase.

These may include:

- Mortgage agreement

- Promissory note

- Closing disclosure

- Property title documents

You’ll also pay any closing costs and your remaining down payment.

Once everything is signed and processed, the home is officially yours.

Typical Closing Costs in Indiana

Closing costs usually range from 2% to 5% of the home price.

These costs may include:

- Loan origination fees

- Title insurance

- Appraisal fees

- Property taxes

- Recording fees

Your lender will provide a closing disclosure at least three days before closing so you know exactly what to expect.

Getting the Keys

After signing the paperwork and completing the transaction, you’ll receive the keys to your new home.

It’s a moment that makes the entire mortgage process worth it.

Tips for Navigating the Mortgage Process in Indiana

Buying a home is a major financial decision, so it helps to approach the process with preparation and patience.

Here are some helpful tips for Indiana homebuyers.

Improve Your Credit Before Applying

A higher credit score can lead to lower interest rates and better loan terms.

Even a small improvement can save thousands of dollars over the life of the mortgage.

Save for Unexpected Costs

Homeownership includes expenses beyond the mortgage payment, such as:

- Maintenance

- Repairs

- Property taxes

- Insurance

Having an emergency fund can make these costs easier to handle.

Work With Local Experts

Local lenders and real estate agents understand the Indiana housing market better than national companies.

They can guide you through the process and help you avoid common pitfalls.

Be Patient

Mortgage approvals involve many moving parts, from inspections to underwriting.

Staying organized and responsive to your lender can help keep things moving smoothly.

Final Thoughts

Understanding the 5 stages of a mortgage in Indiana can make the homebuying journey much less intimidating.

From mortgage pre-approval to closing day, each stage plays an important role in helping you secure financing and purchase your home.

Here’s a quick recap of the stages:

- Mortgage Pre-Approval

- House Hunting and Offer

- Mortgage Application

- Loan Processing and Underwriting

- Closing

While the mortgage process may seem complicated at first, breaking it down step by step makes it much easier to manage.

With the right preparation, guidance, and patience, you’ll be well on your way to becoming a homeowner in Indiana.

And when you finally unlock the door to your new home, every step of the journey will feel completely worth it.