If you’re a homeowner in Indiana and you’ve been thinking, “There has to be a way to use the equity in my home without selling it,” you’re not alone. A second mortgage in Indiana can be a practical way to access cash for big goals — whether that’s renovating your kitchen, paying off high-interest debt, covering college tuition, or handling unexpected expenses.

But before you sign anything, it’s important to really understand how a second mortgage works, what it costs, and whether it’s the right move for you. Let’s break it down together in simple, no-nonsense terms.

Table of Contents

What Is a Second Mortgage?

A second mortgage is a loan that uses your home as collateral — just like your original (first) mortgage. The difference? It’s “second” because your primary mortgage gets paid first if something goes wrong and the home is sold.

In Indiana, second mortgages are commonly taken out as:

- Home equity loans

- Home equity lines of credit (HELOCs)

Both options let you borrow against your home equity — which is the difference between what your home is worth and what you still owe on your first mortgage.

For example, if your home in Indianapolis is worth $300,000 and you owe $200,000, you may have $100,000 in equity. A lender might allow you to borrow a portion of that.

How Does a Second Mortgage Work in Indiana?

When you take out a second mortgage in Indiana, you’re essentially adding another monthly payment on top of your existing mortgage. You’ll continue paying your first mortgage as usual, and now you’ll also pay the second loan.

Here’s what typically happens:

- A lender evaluates your credit score, income, debt, and home value.

- They determine how much equity you can borrow against.

- You receive funds either as a lump sum (home equity loan) or as a revolving credit line (HELOC).

- You repay the loan over time, with interest.

Indiana lenders usually allow homeowners to borrow up to 80–85% of their home’s value (combined loan-to-value ratio), but exact limits vary by lender.

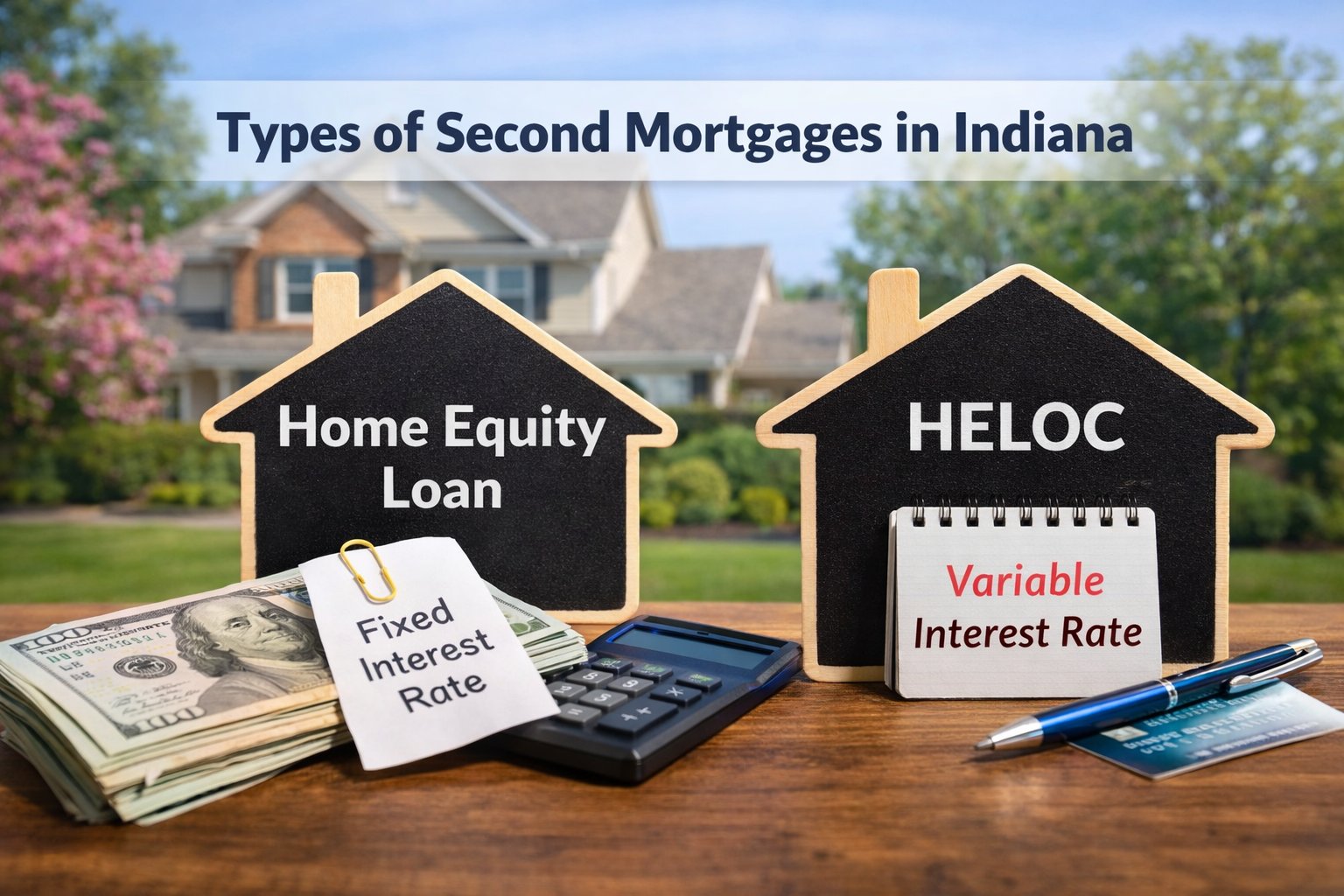

Types of Second Mortgages in Indiana

1. Home Equity Loan (Fixed-Rate Option)

A home equity loan gives you a lump sum upfront. You’ll repay it in fixed monthly payments over a set term — usually 5 to 20 years.

This option is ideal if:

- You know exactly how much money you need.

- You’re funding a specific project like a home remodel.

- You prefer predictable monthly payments.

Because the interest rate is typically fixed, your payment won’t change — which can be comforting if you like stability.

2. HELOC (Home Equity Line of Credit)

A HELOC works more like a credit card. You’re approved for a credit limit and can draw from it as needed during the “draw period.”

This option may work well if:

- You need flexibility.

- You’re covering ongoing expenses (like phased renovations).

- You want to borrow gradually.

Keep in mind that most HELOCs in Indiana have variable interest rates, which means your payment can fluctuate.

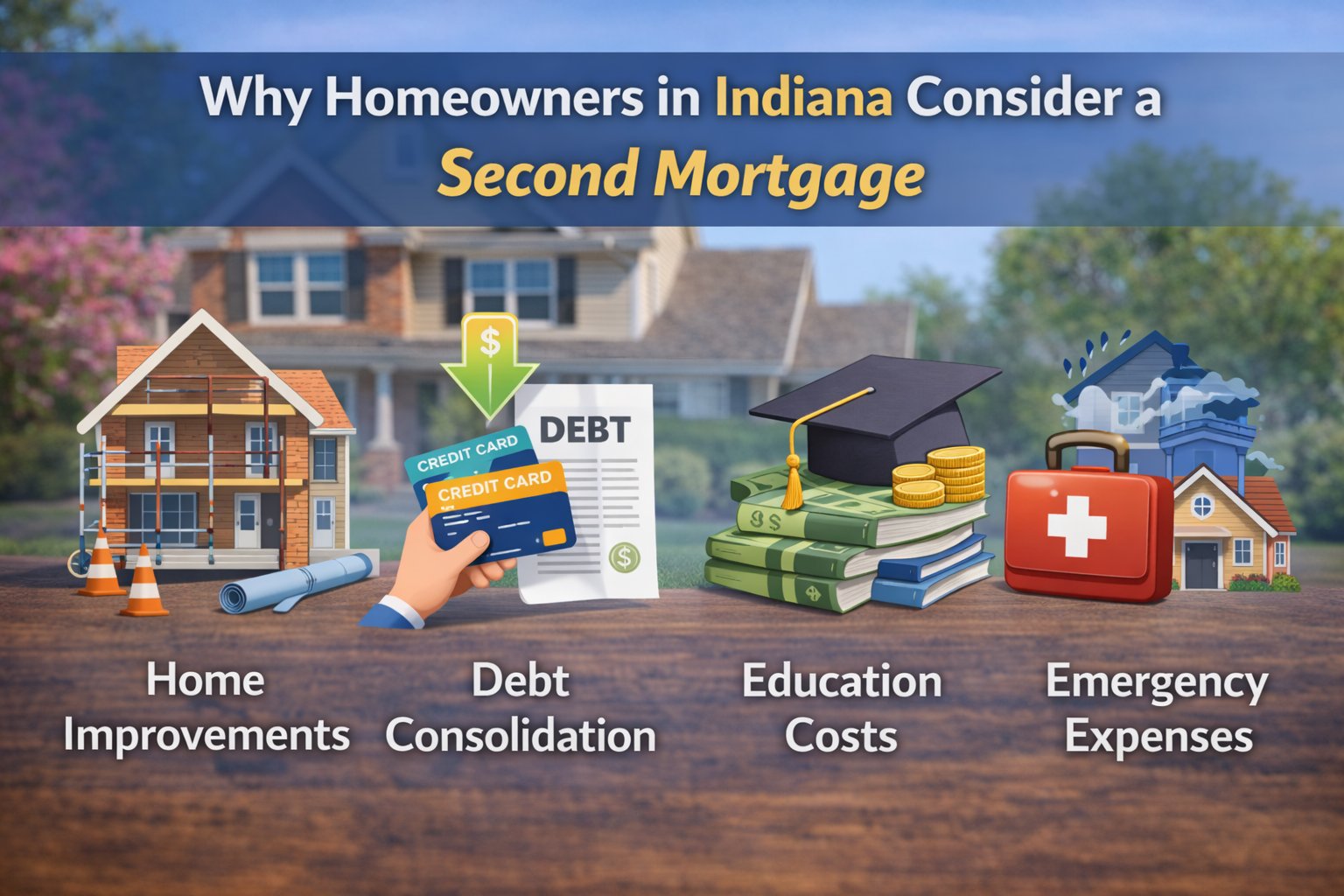

Why Homeowners in Indiana Consider a Second Mortgage

Let’s be honest — life gets expensive. Here are some of the most common reasons Indiana homeowners look into a second mortgage:

🏡 Home Improvements

From upgrading your kitchen in Carmel to finishing your basement in Fort Wayne, renovations can increase your home’s value and improve your daily life.

💳 Debt Consolidation

If you’re juggling high-interest credit cards, using a second mortgage to consolidate debt could lower your interest rate and simplify payments.

🎓 Education Costs

College tuition isn’t cheap. Some homeowners tap into equity to help their children avoid high-interest student loans.

🚑 Emergency Expenses

Unexpected medical bills or major repairs can hit hard. A second mortgage can provide breathing room.

Requirements for a Second Mortgage in Indiana

While every lender is different, most Indiana lenders look for:

- Credit score: Typically 620 or higher (higher scores get better rates).

- Stable income: You must show you can handle two mortgage payments.

- Equity in your home: Usually at least 15–20%.

- Reasonable debt-to-income ratio (DTI): Ideally below 43–45%.

You’ll also likely need:

- A home appraisal

- Income documentation (W-2s, tax returns)

- Proof of homeowner’s insurance

Pros of Getting a Second Mortgage

Let’s talk about the upside.

✔ Lower Interest Rates Than Credit Cards

Because your home secures the loan, rates are usually much lower than personal loans or credit cards.

✔ Access to Larger Loan Amounts

You may qualify for more money compared to unsecured loans.

✔ Potential Tax Benefits

In some cases, interest may be tax-deductible if used for home improvements (check with a tax professional).

✔ Keep Your First Mortgage Rate

If you locked in a great first mortgage rate (say 3%), a second mortgage allows you to access equity without refinancing the entire loan at today’s higher rates.

Cons You Shouldn’t Ignore

Now for the reality check.

❌ Your Home Is at Risk

If you can’t make payments, you could face foreclosure. This is serious.

❌ Additional Monthly Payment

You’re adding another financial obligation.

❌ Closing Costs

Yes, there are usually fees involved — appraisal fees, origination fees, and more.

❌ Variable Rates (for HELOCs)

If rates rise, your payments may increase.

It’s important to weigh these risks carefully before moving forward.

Is a Second Mortgage Better Than Refinancing?

This is one of the most common questions homeowners in Indiana ask.

If your current mortgage rate is much lower than today’s rates, refinancing might mean replacing your low-rate loan with a higher one. In that case, a second mortgage could make more sense.

However, if interest rates drop or you want to simplify to one payment, refinancing could be the better move.

It really depends on:

- Your current interest rate

- How much cash you need

- How long you plan to stay in your home

- Your overall financial situation

Talking to a local Indiana mortgage professional can help clarify your options.

What About Indiana Laws and Regulations?

Indiana follows standard mortgage lending practices, but lenders must comply with state and federal regulations. Home equity loans and HELOCs are governed by consumer protection laws that require:

- Clear disclosure of loan terms

- Transparent interest rate details

- Explanation of fees

You also have a right of rescission (usually three business days) after signing certain home equity agreements. That means you can cancel if you change your mind.

Tips Before You Apply for a Second Mortgage in Indiana

If you’re seriously considering it, here are a few practical tips:

1. Check Your Credit First

Review your credit report and correct any errors before applying.

2. Compare Multiple Lenders

Don’t just go with the first bank you find. Compare local Indiana banks, credit unions, and online lenders.

3. Understand the Total Cost

Look beyond the interest rate. Ask about:

- Closing costs

- Annual fees (for HELOCs)

- Prepayment penalties

4. Borrow Only What You Need

Just because you qualify for $80,000 doesn’t mean you should take it.

5. Have a Repayment Plan

Make sure you can comfortably afford both mortgage payments — even if life throws you a curveball.

Who Should Consider a Second Mortgage?

A second mortgage in Indiana may make sense if:

- You have significant equity.

- Your first mortgage rate is low.

- You have a stable income.

- You’re using the funds for a strategic purpose (like improving your home or consolidating high-interest debt).

It may not be a good idea if:

- You’re already struggling with debt.

- Your income is unstable.

- You’re planning to move soon.

- You’re using it for non-essential spending.

Final Thoughts: Is a Second Mortgage in Indiana Right for You?

At the end of the day, a second mortgage in Indiana isn’t just about numbers — it’s about your life, your goals, and your financial peace of mind.

Used wisely, it can be a powerful tool. It can help you upgrade your home, reduce high-interest debt, or cover important expenses without selling your property. But it also comes with responsibility and risk.

Before making a decision, take a deep breath and ask yourself:

- Can I comfortably afford the payments?

- Is this loan helping me move forward financially?

- Do I fully understand the terms?

If the answer is yes, a second mortgage could be the solution you’ve been looking for.

If you’re unsure, that’s okay too. It’s better to pause and gather information than rush into a decision involving your home.

Your house isn’t just a financial asset — it’s where life happens. Make sure any decision you make protects both your investment and your peace of mind.

If you’d like help comparing options, estimating payments, or understanding Indiana home equity loan requirements more deeply, I’m here to help you sort through it step by step.